Vikas Jha, an accomplished leader with over two decades of experience in financial services, brings a wealth of expertise to his role as SEO of Finneva (Finneva is the brand name of MeCred (DIFC) Ltd., a regulated fintech based in DIFC). With a track record of driving innovation at major institutions such as Emirates NBD, DBS Bank India, HSBC, and ICICI Bank, Vikas has successfully transitioned from traditional banking to the fintech sphere. His leadership reflects a commitment to solving the region’s $250 billion SME funding gap through technology-driven solutions.

In this exclusive interview, Vikas shares insights into his journey, the motivation behind Finneva, and his vision for the future of SME financing in the Middle East. From spearheading tailored trade finance solutions to embracing AI and blockchain, Vikas is redefining how financial inclusion and operational efficiency can coexist in the rapidly evolving fintech landscape.

Having held senior roles in traditional banking institutions, what motivated your transition to leading a fintech firm like Finneva?

Two key factors drove my transition. In traditional banking, my focus was on corporate and transaction banking, where responsibilities are often limited to specific areas. While working at Emirates NBD, I noticed many SMEs seeking funding but lacking comprehensive end-to-end solutions.

Fintech offered an exciting opportunity to address this. First, it provides greater control over both product and technology, enabling meaningful innovation. In large banks, driving change can be challenging, though they often do excellent work. Second, fintech involves broader responsibilities—covering relationship management, product development, technology, compliance, and credit—which makes the work dynamic and fulfilling.

Creating products from scratch and seeing their direct impact on customers is incredibly rewarding. This opportunity to innovate and experiment while making a tangible difference is what truly inspired me to make the shift.

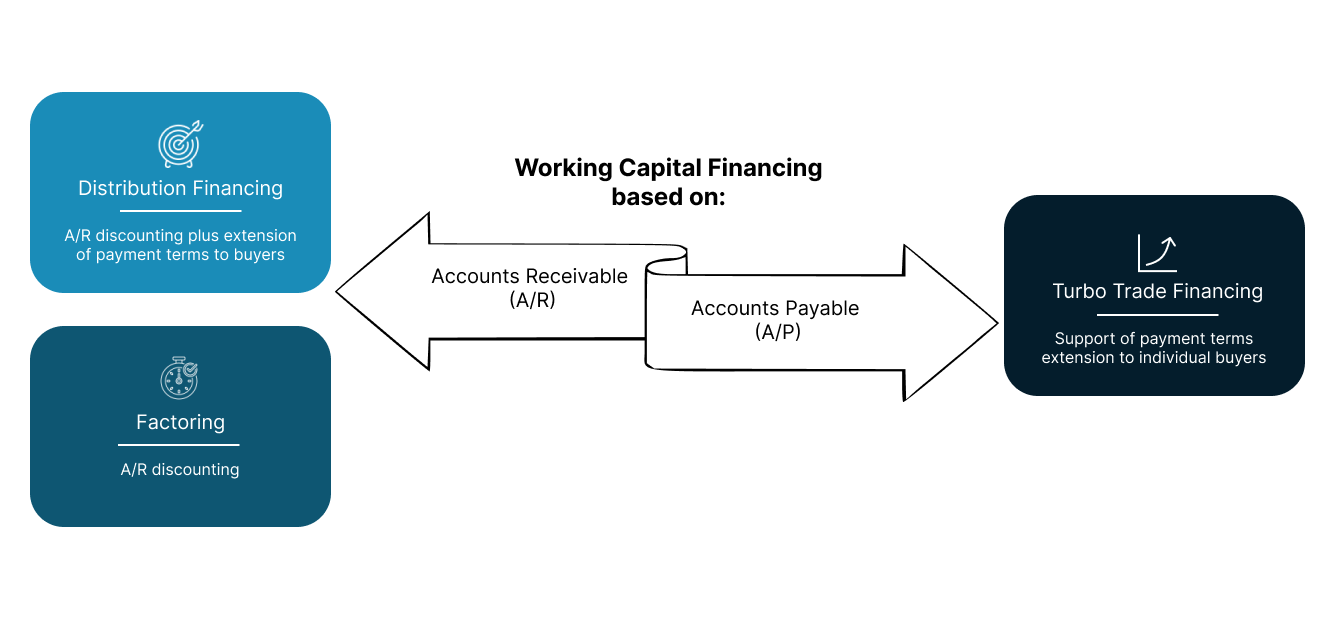

What inspired the creation of Finneva, and how does it differentiate itself from traditional working capital solutions available to SMEs in the Middle East?

Finneva was created to address the substantial $250 billion SME funding gap in the region. Banks often hesitate to finance SMEs due to small ticket sizes, making such transactions less lucrative. This created a clear need for a player to bridge the gap between banks, operational processes, and SMEs. Drawing inspiration from successful fintech solutions globally, we saw an opportunity to introduce Finneva as a comprehensive solution in this part of the world.

Unlike traditional consultancies that only advise, Finneva is action-oriented. We manage the entire operational journey—from deal origination, arranging funding, and processing transactions to monitoring, reconciliation, and collections. This ensures SMEs receive complete support while banks benefit from cost-efficient and streamlined operations.

Our key differentiators are threefold. First, we rely on proprietary technology, developed in-house at our tech office in India, which we tailor for banks and SMEs. Second, we oversee both transactions and operations, offering an end-to-end solution few fintechs provide. While elements of our services exist in the market, fully integrated solutions like ours are rare. Finally, we recognize the enormous size of the SME funding gap, which allows multiple players to collaborate in addressing this critical challenge. By combining technology, operations, and a holistic approach to SME funding, Finneva delivers real, actionable solutions to a pressing regional problem.

Given the regulatory landscape in DIFC, what challenges did you face in structuring Finneva’s offerings, and how did you navigate them?

Adapting to the constantly evolving regulatory environment is an ongoing challenge for SMEs, banks, and fintechs alike. For Finneva, the focus on supply chain financing presented additional complexities due to the bespoke nature of supply chains, which differ significantly between industries like textiles, food, and healthcare. The key challenge was designing tailored solutions that were simple enough for customers while structured to meet the financing requirements of various banks. Simplifying these complex processes and delivering them efficiently at scale was a critical task, especially given the granular and operationally intensive nature of these transactions.

Data management posed another significant challenge. While the government’s initiative on open banking is promising for the future, we currently rely on manual data aggregation, verification, and presentation to banks. This process is resource-intensive but vital for enabling informed decision-making. Despite these hurdles, we’ve leveraged the resources at our disposal and implemented innovative solutions to overcome them. This approach has allowed us to design scalable, efficient offerings that bridge the gap between SMEs and financial institutions.

Can you shed some light on the resource management to address these challenges?

First and foremost, you need to acknowledge that you can’t do everything on your own—you have to be pragmatic. It’s important to identify which challenges you can tackle directly and where partnerships are necessary. For instance, onboarding is a significant challenge, involving compliance and credit checks. We collaborate with partners who excel in compliance checks, integrating their services through APIs. Similarly, for credit, while we have our own credit engine and policy, tasks like data scraping are through various partners.

While we rely on these partnerships, what remains central is the code, design philosophy, tech framework, credit management philosophy, and overall processing. We own the vision and the execution strategy, but we also work with fintech partners in the background to bring efficiency.

Finneva leverages digital solutions for trade financing. What role does AI or blockchain play in your operations at Finneva, and do you see these technologies shaping the future of trade finance?

At Finneva, innovative new technologies are central to our operations, driving efficiency and trust in trade finance. Finneva is a member of Haifin which is a blockchain consortium of 18 financial services companies in UAE and addresses complex challenges, such as duplicate financing. Such initiatives not only build trust among financial institutions but also make it easier for credible SMEs to secure financing and grow.

AI is equally transformative, particularly in areas like credit management, onboarding, and generating insights for both SMEs and financiers. It automates data-intensive tasks, enabling seamless processing and faster decision-making. For instance, customer verifications, which currently require contacting call centers, can be streamlined with AI tools. Additionally, AI helps us manage large datasets and assist rule-based processing, which is critical in trade finance involving numerous documents and data points.

Looking ahead, AI will continue to revolutionize the sector. Complex data challenges and routine tasks, such as analyzing trade documents and making credit decisions, will become significantly easier. Within the next 2–3 years, I envision AI addressing key pain points like data processing, customer service, and credit decisioning. These advancements will complement our current systems and play a vital role in addressing the SME financing gap in the region.

What is Finneva’s approach to risk assessment for SMEs that may lack traditional credit histories? Are alternative credit scoring models being explored?

Finneva adopts a comprehensive risk assessment model that goes beyond the traditional reliance on financial statements and past performance. While financial data remains a factor, we take a 360-degree view, incorporating trade data, counterparty relationships, the nature of the business, and industry trends to create a well-rounded evaluation.

Our focus is on understanding the SME's growth potential and the financing required to support that growth. Unlike traditional methods, which prioritize historical data, we emphasize how financing can enable future scalability. For example, SMEs in the food sector, such as those supplying to major retailers like Carrefour or Lulu, often experience annual growth rates of 20–30%. Their financing needs evolve significantly year-on-year, and our approach accounts for this dynamic growth rather than limiting decisions to past data.

This tailored methodology allows us to design solutions that address current and future financing challenges, making Finneva’s approach more flexible and growth-oriented compared to traditional financing models.

Is this approach the same across different stages, like a relatively new startup?

The approach remains the same, but the way data is analyzed differs. For instance, whether it’s the healthcare sector, the tech industry, or a restaurant business, the method of evaluating financial data will vary slightly based on the nature of the business. However, the core approach is consistently always growth-focused.

While we do consider the SME’s past track record, the primary focus is on identifying opportunities and enabling the SME to secure the financing they need to grow. Ultimately, as they grow, we grow with them.

What markets or industries do you see as the biggest opportunities for Finneva’s expansion beyond the UAE?

For the next two to three years, Finneva’s primary focus will remain on the UAE, where over half a million SMEs present a significant opportunity. Beyond the UAE, the MENA region offers natural expansion opportunities due to the similarity in supply chains across countries such as KSA, Egypt, Oman, Qatar, and Kuwait. While the business model can largely remain the same, adjustments will be necessary to align with local regulatory frameworks and business practices.

Finneva is currently focused on five key industries: healthcare, education, food and FMCG, technology (covering both IT distribution and technology as a service), and manufacturing. However, our approach is dynamic, and we are open to exploring additional sectors where our solutions can provide significant benefits to SMEs. Our strategy is to grow strategically, expanding into markets and industries where we can drive meaningful impact while supporting SME growth.

Many fintechs face challenges in customer acquisition. What strategies is Finneva using to build trust and onboard SMEs efficiently?

Finneva employs a hybrid approach, blending digital efficiency with physical interactions to build trust. While digital tools streamline processes, the relationship-building aspect remains physical to address SMEs' critical need for confidence. Meeting clients in person allows us to understand their unique needs and tailor solutions accordingly, which is key to fostering long-term relationships.

Our acquisition strategy is primarily driven by word-of-mouth referrals and anchor corporates. Delivering value to one SME often leads to referrals to others, as the SME community in the UAE remains well-connected. Anchor corporates also play a significant role, introducing us to their SME networks when satisfied with our services.

We focus on digital client journeys and leveraging our proprietary technology to solve complex operational challenges in a phased manner. Ultimately, while digital tools lower entry barriers, physical interactions remain vital for understanding SME pain points and delivering customized solutions, as a one-size-fits-all approach doesn’t work in this space. Quality service and strong relationships are at the core of our strategy to overcome customer acquisition challenges.

How much capital has Finneva facilitated for SMEs so far, and what are your targets for the year?

We are a growing company, well-financed, and with large aspirations. In our first year, we are working with clients in our selected sectors having arranged financial services for their growth ambitions, and this number continues to grow daily. Looking ahead, our goal for the next 18 to 24 months is to facilitate roughly USD 1 billion in financing for SMEs, potentially impacting around 250 to 300 businesses.

From a long-term perspective, over the next 36 months, we aim to influence and impact 1% of the SME financing gap in the region. With the gap estimated at USD 250 billion, this translates to facilitating around USD 3 billion. It’s an ambitious goal, but we are confident in our ability to achieve it.

What gives us confidence is our strong foundation. We are a regulated entity, well-capitalized, and have an experienced team with deep connections to local and international funders. Our team’s understanding of SMEs, sector, credit, product and processes, combined with actionable insights and in-house technology, positions us to address this challenge effectively. While it’s an aspirational target, we are committed to working hard and achieving it.

You described 2025 as the year of Scale, Continued Momentum, and Progress Towards our Vision. In what measurable ways do you plan to recognize these goals by the final quarter of this year?

Over the past year and a half, we have laid the foundation for our products and technology. We’ve tested various approaches, identifying what works and, more importantly, what doesn’t. While theoretical knowledge can guide us, real-world application often reveals unexpected challenges. Through multiple cycles of transactions, we’ve refined our focus and now have a clear understanding of where to concentrate our efforts.

This year is about showcasing our capabilities and accelerating growth. For instance, as I mentioned earlier, our goal over the next 18 months is to facilitate USD 1 billion in financing for SMEs. The challenge lies in scaling our operations while maintaining the high service standards we’ve established.

Now that we have the key elements—products, partnerships, and technology—our focus is on effective marketing and outreach. We aim to expand our customer base and onboard more SMEs and financiers, ensuring that our growth remains sustainable and impactful. The progress we’ve made so far is the result of hard work, and 2025 will be about leveraging these foundations to achieve our ambitious goals.

Right now, your product is geared towards SMEs. Is there a possibility that in the future you would expand the services you provide to corporate entities as well?

Just a minor clarification—when we work with SMEs, we are addressing the supply chain ecosystem, which inherently involves both SMEs and corporates. Our solutions are designed to ensure that corporates benefit as well, such as receiving better, just-in-time products through an improved supply chain. While SMEs are directly impacted, there is also an indirect impact on the corporates linked to these supply chains.

In this region, many corporates, especially larger ones, are already well-banked. Our focus has been on mid-market corporates, some of whom have already approached us for solutions. While we are working with them to an extent, our primary focus will remain on SMEs for at least the next 2–3 years.

It’s not a "never" scenario, but given the scale of the SME financing challenge and our current resources, we are dedicated to addressing SME needs in the near term. Ultimately, we hope that the growth and success of SMEs will create a positive ripple effect, indirectly benefiting the larger corporates as well.

Also Read:

![Interview with Nader Bassit, CEO of El Greco Restaurant [Wakira Investments] in Dubai](/content/images/size/w300/2023/08/Untitled-design--1-.jpg)