Every business in Dubai hits a slow patch eventually. A major client leaves, a contract gets delayed, a market shifts. The revenue dips, the pressure mounts — and the instinct is to focus entirely on sales recovery while quietly hoping the financial obligations manage themselves.

They don't.

What many business owners discover too late is that a period of low revenue doesn't just strain the bank account. It leaves a trail on your Al Etihad Credit Bureau (AECB) file, the official record that every bank, major supplier, and government entity in the UAE consults before deciding whether to do business with you, and on what terms.

The AECB, established under UAE Federal Law No. 6 of 2010, scores businesses on a scale of 300 to 900. That number follows your company into every loan application, every lease renewal, and every tender submission. Damage it during a difficult quarter, and you may find the recovery period far longer than the downturn itself.

This article is a practical guide to protecting that score when cash flow gets tight what to pay first, how to talk to your bank before things escalate, and how to avoid the specific mistakes that do the most lasting damage in the UAE credit system.

The AECB Framework: Understanding What Shapes Your Score

The AECB credit score for businesses operates on a scale of 300 to 900. A higher score signals lower credit risk. The following table illustrates the scoring tiers and their general implications for business credit access:

| Score Range | Rating Category | General Implication |

|---|---|---|

| 750 – 900 | Excellent | Access to best available financing terms; strong lender confidence |

| 650 – 749 | Good | Eligible for most credit products; minor scrutiny from lenders |

| 550 – 649 | Fair | Lenders may apply stricter conditions; higher interest rates possible |

| 450 – 549 | Poor | Credit access is limited; collateral or guarantees often required |

| 300 – 449 | Very Poor | Most mainstream credit facilities are unavailable; serious remediation required |

These tiers are not rigid boundaries that all financial institutions apply uniformly. Each bank and financing institution applies its own internal risk policies on top of the AECB score. However, the score provides the baseline signal that shapes every initial credit decision.

Data Points the AECB Collects

Understanding what data feeds your score is the first step in managing it intelligently. The AECB draws information from a broad range of public and private reporting entities. These include:

Banking and Financial Data:

- All active and closed credit facilities (term loans, revolving credit, trade finance lines, overdrafts)

- Payment history on each facility, including dates and amounts of missed or late payments

- Utilization levels on revolving credit products

- Guarantees given on behalf of other parties

- Legal proceedings initiated by financial institutions

Utility and Telecommunications Data: The AECB also integrates data reported by utility and telecoms providers. This is a dimension that many business owners underestimate. Providers, including DEWA (Dubai Electricity and Water Authority), SEWA (Sharjah Electricity and Water Authority), Etisalat (now e&), and du, report payment behaviour to the AECB. Consistent late payment on a DEWA corporate account, for example, can negatively affect your credit score even if your bank repayments are current. This integration reflects the UAE's intention to create a comprehensive financial reliability profile for every business in the system.

Cheque Data: The AECB operates a dedicated ChequeScore system that captures all dishonoured cheque events. This is covered in detail in a later section, but it is important to note at this stage that cheque data is a distinct and significant component of your overall credit profile.

Public Records: Court judgements, insolvency proceedings, and formal legal actions are also recorded in the AECB database.

How the AECB Score Is Used

Banks licensed by the UAE Central Bank are required to consult AECB data as part of their credit evaluation process. This obligation extends to the assessment of both new credit applications and annual reviews of existing facilities. A deteriorating score during a period of low revenue can therefore trigger a review of facilities you already hold, not just affect your ability to access new ones.

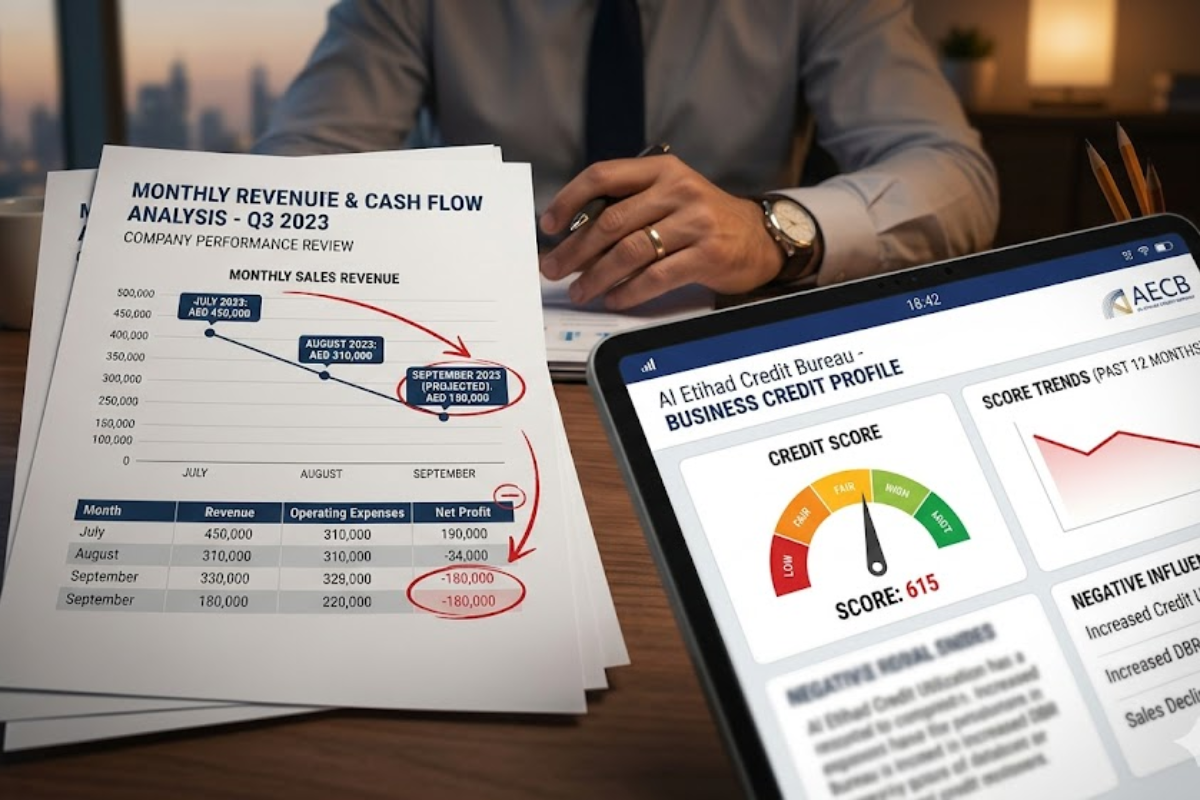

The Mechanics of a Sales Slump: How Declining Revenue Damages Your Score

The Debt Burden Ratio (DBR) is a core metric used by UAE banks and credit assessors to evaluate a business's repayment capacity. It measures the proportion of income that is committed to servicing existing debt obligations. The UAE Central Bank has established regulatory guidelines around DBR thresholds for retail lending, and commercial lenders apply similar logic to business credit assessments.

When revenue declines, the DBR deteriorates even if the absolute level of debt remains unchanged. A business generating AED 500,000 per month in revenue with AED 200,000 in monthly debt obligations carries a DBR of 40%. If revenue falls to AED 300,000 while debt service remains AED 200,000, the DBR rises to approximately 67%. That shift communicates a fundamentally different risk profile to a lender reviewing your account.

Credit Utilization and Its Scoring Impact

Credit utilization, the percentage of an available revolving credit line that is currently drawn, is a significant factor in credit scoring. During revenue downturns, businesses frequently draw down on overdrafts and credit lines to bridge cash flow gaps. High utilization, particularly utilization consistently above 70–80% of the available limit, signals financial strain to credit assessment systems and can depress your score even when payments are technically being made on time.

The Payment History Cascade

Payment history is the single most heavily weighted factor in most credit scoring models. A single payment that is reported as more than 30 days overdue can cause a measurable drop in your AECB score. Multiple delinquencies across different facilities can trigger a cascade that moves a business from the "Good" tier to the "Poor" tier within two to three reporting cycles. The damage is asymmetric: it takes months of consistent positive behaviour to recover the score points that a single reported delinquency removes.

Immediate First Aid Steps

Step 1: Prioritise Your Payments by Impact Level

Not all financial obligations carry the same consequences for your credit score if they fall behind. During a period of constrained cash flow, you must triage your payment obligations intelligently. The following table provides a priority framework:

| Priority Level | Obligation Type | Reason for Priority |

|---|---|---|

| Critical | Bank loan repayments and credit facility instalments | Directly reported to AECB; triggers formal delinquency after 30 days |

| Critical | Post-dated cheques presented for clearance | Bounced cheques generate a ChequeScore event immediately |

| High | Overdraft interest and fees | Non-payment can trigger facility review and potential cancellation |

| High | DEWA, SEWA utility accounts | Reported to AECB; affects utility account status and credit score |

| High | Etisalat / du corporate accounts | Reported to AECB; late payment affects telecommunications credit data |

| Medium | Trade supplier invoices (non-bank) | Not directly AECB-reported but affects trade relationships and references |

| Lower | Internal operational expenses | No direct AECB reporting; manage by renegotiating terms with vendors |

This prioritisation is not an instruction to ignore lower-priority obligations. It is a recognition that in a cash-constrained environment, the sequence in which you allocate available funds has direct consequences for the formal credit record that follows your business.

Step 2: Navigate the 30-Day Reporting Window

UAE banks typically report payment delinquency to the AECB after a payment has been outstanding for 30 days past its contractual due date. This window is operationally important. A payment that is made late but within the 30-day window may not appear as a formal delinquency on your AECB report, depending on the reporting cycle of the specific institution.

Key actions to take within this window:

- Contact your relationship manager immediately when you anticipate a missed payment. Do not wait until the due date passes.

- Make a partial payment if the full amount is unavailable. Demonstrating intent and partial compliance can support your position in any subsequent bank conversation.

- Document the communication in writing. An email or formal letter to the bank stating the reason for the delay and the expected resolution date creates a record that supports your case during any internal review.

- Request a formal payment deferral in writing, citing the specific facility and the amount. Some banks will issue a formal deferral notice, which prevents the account from moving into delinquency status during the agreed period.

The 30-day window is not a grace period in the legal sense. Its existence and parameters vary by institution and facility type. Treat it as an operational buffer, not a right.

Step 3: Proactive Communication Requesting Restructuring Without Triggering "Legal" Status

The most damaging marker on an AECB business credit report is a "Legal" classification. This status is applied when a bank has commenced formal legal proceedings against a borrower, typically after all other recovery attempts have failed. A Legal classification on your AECB file will effectively shut your business out of the formal banking system for the duration of the proceeding and for a significant period afterward.

Restructuring, on the other hand, is a legitimate and recognized mechanism under UAE banking practice. A restructured facility indicates that the bank and the borrower have agreed to modify the original repayment terms, typically by extending the tenure, adjusting the instalment amount, or providing a temporary payment holiday. A restructured classification is not neutral on your credit report, but it is substantially less damaging than a Legal classification and signals that the situation is being managed responsibly.

How to approach a restructuring conversation:

- Request a formal meeting with your relationship manager or branch manager. Do not conduct this conversation informally.

- Prepare a clear financial summary before the meeting: current revenue figures, projected recovery timeline, assets held with the bank, and total facilities outstanding.

- Use the correct terminology. Request a "restructuring" or "rescheduling" of your facility. Avoid language that suggests you are unable to repay entirely.

- Submit a written request that outlines the proposed new terms, the reason for the request, and the business plan supporting recovery. Banks are required by UAE Central Bank regulations to evaluate restructuring requests from business clients in good faith.

- Engage a financial advisor or legal consultant if the facilities are large or if the bank's initial response is non-cooperative. Structured professional engagement signals seriousness and often accelerates internal bank processes.

A business that proactively manages its banking relationships during a downturn consistently achieves better outcomes than one that avoids communication until the situation has become unmanageable.

The Bounced Cheque Factor: Protecting Your ChequeScore

The post-dated cheque remains a foundational instrument in UAE commercial transactions. Landlords, suppliers, and government entities routinely require post-dated cheques as a form of payment commitment or security. This commercial practice means that a business carrying multiple outstanding post-dated cheques has, in effect, pre-committed future cash flows at a time when those cash flows are uncertain.

Under UAE law, a dishonoured cheque is not merely a commercial inconvenience. Federal Law No. 18 of 1993 (the UAE Commercial Transactions Law, as amended) and subsequent penal code provisions have historically treated cheque dishonour as a criminal matter. While legislative reforms in recent years have modified aspects of the criminalisation framework, particularly for cheques that are immediately followed by settlement, the reputational and credit consequences of a bounced cheque remain severe.

The AECB ChequeScore

The AECB operates a dedicated ChequeScore system that records all dishonoured cheque events reported by UAE banks. A ChequeScore event is generated when a cheque is returned unpaid and recorded by the presenting bank. The ChequeScore is separate from but linked to the main AECB credit score, and lenders, landlords, and counterparties can access it as an independent data point when assessing your business.

A single dishonoured cheque, even if subsequently settled, leaves a permanent record in the AECB system for a defined period. Multiple dishonoured cheque events signal serious financial instability and will materially damage your ability to secure banking facilities, renew commercial leases, and maintain supplier relationships.

Strategies to Protect Your ChequeScore During a Cash Flow Squeeze

1. Conduct a Cheque Exposure Audit

Immediately, list every post-dated cheque you have issued that has not yet cleared. Record the payee, the amount, the presenting date, and the bank account from which it will be drawn. This audit gives you a complete picture of your near-term cheque obligations.

2. Match Cheque Dates to Cash Flow Projections

Map each upcoming cheque against your realistic cash flow timeline. Identify which cheques are at risk of dishonour before their presentation date, not after.

3. Contact Payees Before Presentation

If a cheque is at risk, approach the payee before the presentation date to discuss replacement, deferral, or alternative payment. A payee who agrees to hold a cheque for a later date or accept a bank transfer in lieu has eliminated the cheque risk. This requires proactive, honest communication.

4. Request Cheque Return or Cancellation

In some commercial relationships, payees will agree to return a post-dated cheque in exchange for a formal payment plan or a different instrument. This eliminates the dishonour risk entirely. Get any such agreement in writing.

5. Prioritise Funding the Account Before Presentation

If the cheque cannot be deferred, prioritise funding the bank account from which it will be drawn, even above other payment obligations. The immediate reputational and legal consequences of a dishonoured cheque in the UAE make it one of the highest-priority cash management decisions a business can make.

6. Do Not Issue New Post-Dated Cheques During Uncertainty

During a period of constrained cash flow, avoid issuing new post-dated cheques for commitments that extend beyond your reliable cash flow visibility. Offer alternative payment structures, such as bank transfers, instalment agreements, or other documentary instruments, where counterparties will accept them.

Official Resources: AECB Tools and Dubai SME Support Frameworks

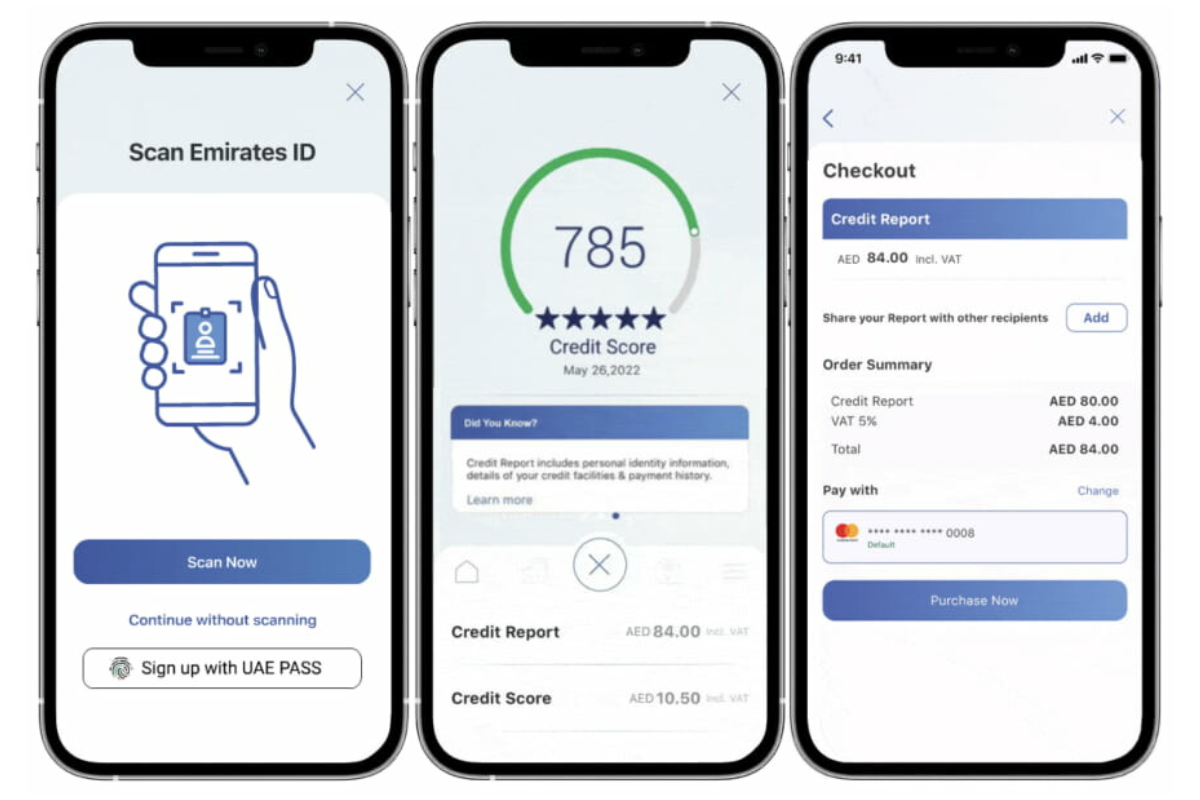

Using the AECB Platform Directly

The AECB provides businesses with direct access to their own credit information through the AECB app and online portal. Business owners and authorised company representatives can:

- Access the full AECB business credit report at any time, giving visibility into exactly what lenders and counterparties see when they conduct a credit check.

- Review the ChequeScore as a standalone report to monitor the status of any cheque-related events.

- Dispute inaccurate data through the formal AECB dispute resolution mechanism. If a payment has been reported as delinquent in error, or if a settled cheque continues to appear as outstanding, the AECB dispute process provides the channel for correction.

- Monitor score changes over time to assess the impact of your financial management decisions.

Proactive monitoring of your AECB report is not a reactive measure; it is a standard component of responsible business financial management. Many business owners only consult their AECB report when they are denied credit, which is far too late to address the factors that led to the denial.

A sales slump is a temporary condition. The credit damage it causes, if left unmanaged, can be permanent in its operational consequences. The difference between a business that emerges from a difficult trading period with its credit profile intact and one that spends years rebuilding from a damaged AECB file is not luck; it is the quality of the financial decisions made during the difficult period itself.

Please note: This article is for informational purposes only and does not constitute financial or legal advice. Business owners are encouraged to consult qualified financial advisors and refer to official AECB, UAE Central Bank, and Dubai SME resources for guidance specific to their circumstances.

Also Read: