Opening a business bank account in Dubai has become one of the most scrutinised stages of the entire company setup process, and for good reason. Under the Central Bank of the UAE's updated regulatory framework, banks are operating under significantly tighter compliance obligations.

KYC checks are detailed, documentation standards are high, and the consequences of an incomplete or poorly prepared application are measured in weeks of delay rather than a quick back-and-forth with a relationship manager.

For entrepreneurs and business owners, the good news is that this process is entirely navigable with the right preparation. Banks are not trying to exclude legitimate businesses; they are protecting themselves from regulatory penalties under an environment of stricter anti-money laundering and Know Your Customer enforcement.

Understanding what banks are looking for and presenting your business accordingly is the difference between a smooth approval and a prolonged rejection cycle.

What the Current Regulatory Environment Requires

Several regulatory developments have converged to make the UAE banking environment materially more demanding than it once was. Federal Decree-Law No. 6 of 2025 modernised the UAE's banking framework to incorporate Open Finance services and virtual asset integration, while simultaneously tightening the obligations on financial institutions around customer due diligence. Banks are now required to conduct high-speed digital due diligence, AI-driven risk profiling that assesses a business's activity codes, ownership structure, and digital footprint before a human reviewer even enters the picture.

Two specific changes have had the most direct impact on business applicants. First, virtual office arrangements, previously accepted by many banks as proof of business address, are now subject to significantly stricter scrutiny. Most Tier 1 banks require a physical lease agreement (Ejari) for a dedicated office space, not a flexi-desk or co-working membership. Second, Ultimate Beneficial Owner declarations have become a mandatory and rigorously verified requirement. Any ambiguity in the ownership chain, holding companies, nominee arrangements, or corporate shareholders without clear documentation will stall an application.

Traditional Banks vs Digital Neobanks: Choosing the Right Path

One of the most significant developments in Dubai's banking landscape is the maturation of digital neobanks as a credible alternative to traditional institutions for SMEs and startups. Understanding the distinction between the two paths and which is appropriate for your business profile is one of the first decisions to make.

Traditional Tier 1 banks, including Emirates NBD, ADCB, FAB, and Mashreq, offer long-term credibility, access to trade finance, multi-currency capabilities, and WPS integration mandatory for mainland businesses paying salaries. The trade-off is time and documentation intensity. Approval timelines range from four to eight weeks for straightforward applications, extending further for complex ownership structures or high-risk activity categories. Minimum average monthly balance requirements typically range from AED 50,000 for SME basic accounts to AED 200,000 to AED 500,000 for preferred accounts.

Digital neobanks, including Wio, Zand, and Mashreq NeoBiz, offer a different proposition. Onboarding is predominantly mobile-based, approval timelines are three to ten working days, and minimum balance requirements start from zero on basic plans. For startups in the early stages of building transaction history, or for free zone companies operated by non-resident founders who cannot easily attend in-person interviews, the neobank route provides a practical entry point. Many businesses use a neobank initially to establish operating history, then transition to a traditional bank once their financial profile is more established.

The Document Checklist

Incomplete documentation is the single most common reason for application rejection or delay. The following represents the core document set required by the majority of Dubai banks, with notes on elements that are frequently overlooked.

- Valid UAE trade licence, with activity codes that clearly reflect actual business operations. If your activity code is on a bank's high-risk list, categories including crypto, jewellery, or cross-border trading, expect enhanced due diligence and a longer review timeline.

- Certificate of incorporation and Memorandum and Articles of Association (MOA/AOA), clearly identifying all shareholders and directors.

- Passport copies and Emirates ID (where applicable) for all shareholders, directors, and authorised signatories. For UAE residents, both are required. For non-resident shareholders, passport copies and visa documentation from the home country may be requested.

- Physical office proof; an Ejari tenancy contract for a dedicated office space. For Tier 1 banks in particular, a flexi-desk arrangement or co-working membership is unlikely to be sufficient.

- Six months of personal or corporate bank statements from your home country or existing UAE bank, demonstrating the source of funds and financial history.

- Ultimate Beneficial Owner (UBO) declaration, clearly identifying every individual who ultimately owns or controls more than 25 percent of the company.

- A structured business plan of two to three pages, covering the company's activities, expected annual turnover, primary customers and suppliers, and a clear explanation of how revenue is generated and received. This document carries more weight than most applicants realise.

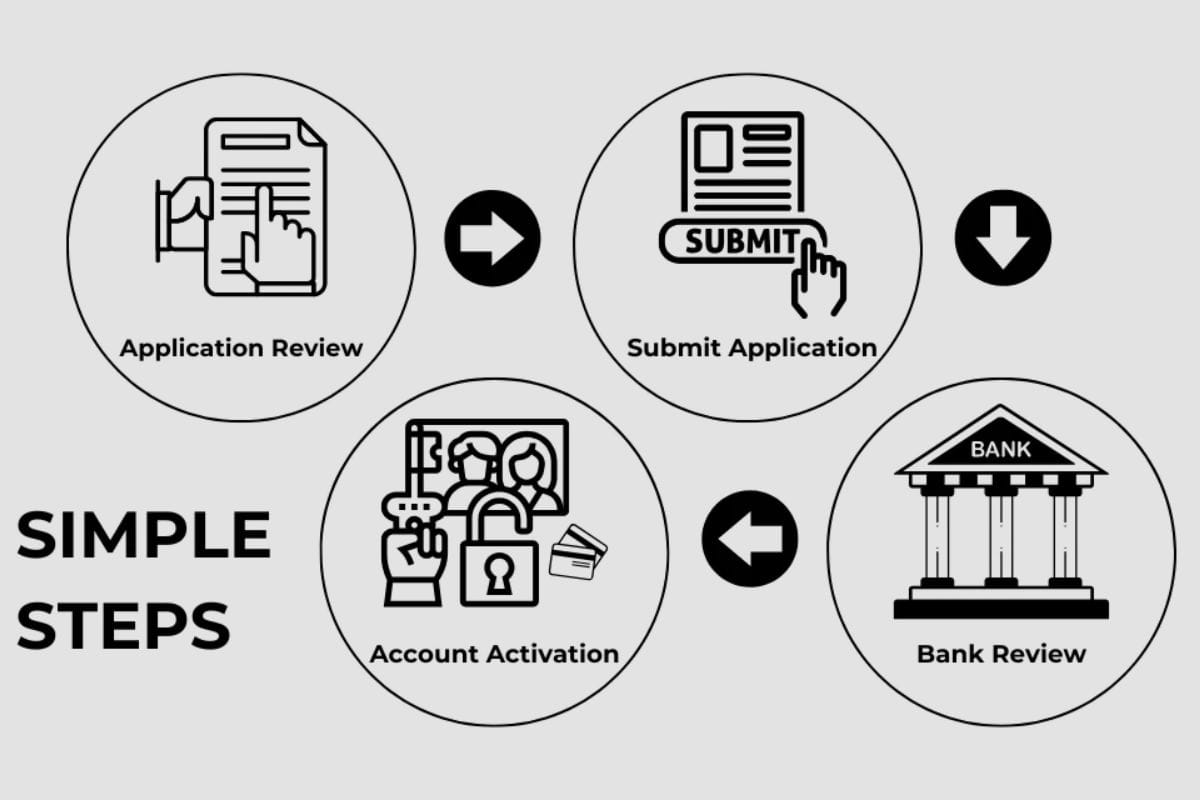

The Application Process Step by Step

- Select your bank based on your business profile.

Match your company type, activity, and ownership structure to the bank most likely to approve it. Startups and free zone companies typically have the strongest outcome with neobanks or startup-friendly traditional banks such as RAKBANK and Mashreq. Larger or more established businesses with complex needs should engage Emirates NBD or FAB.

- Initiate the application digitally

It can be done via the bank's app or portal, where available, using UAE PASS. Many banks now auto-fetch trade licence data from government databases at this stage, reducing manual entry errors.

- Submit the complete document dossier.

Ensure every name, date, and detail is consistent across all documents. Any discrepancy between the trade licence, MOA, and passport details is a common trigger for compliance flags and delays.

- Attend the compliance interview.

For mainland accounts and most Tier 1 bank applications, a brief interview with a relationship manager or compliance officer is required, either in person or via video call. This is where applicants must be prepared to clearly and specifically explain their business model, sources of funds, and expected transaction volumes. Vague or inconsistent answers at this stage are a frequent cause of rejection.

- Fund the account upon approval.

Once the IBAN is issued, ensure the minimum average balance is deposited promptly to avoid fall-below fees. Most banks now support instant payments for immediate account funding.

The Most Common Reasons Applications Are Rejected

Understanding why applications fail is as important as understanding what they require. The most frequently cited rejection reasons are consistent across banks and are largely avoidable with adequate preparation.

- Unclear or vague source of funds.

Banks will not approve accounts where the origin of the initial deposit or operating capital cannot be clearly documented. Employment records, prior business income, investment returns, or property sale proceeds are all acceptable, but they must be evidenced, not described.

- Business model does not match the trade licence activity.

If your application describes a business that operates differently from what your licence activity code permits, banks will flag the inconsistency. Ensure your licence accurately reflects what you actually do.

- No digital presence.

Banks routinely check company websites and social media profiles to verify that the business is operational. A company with no online presence raises credibility concerns that slow or prevent approval.

- Reliance on a virtual office.

For Tier 1 banks, a flexi-desk arrangement without a dedicated Ejari lease is frequently insufficient. If your business is free zone based, check the specific requirements of your target bank before applying.

Costs and Timelines to Plan For

Most banks do not charge an account opening fee, but the associated costs are real and should be factored into business planning from the outset. Compliance review fees range from AED 1,000 to AED 5,000 for more complex applications.

Minimum average monthly balance requirements range from AED 25,000 to AED 150,000 for standard SME accounts at traditional banks, with preferred tier accounts requiring AED 200,000 to AED 500,000.

Neobank basic plans may carry zero minimum balance obligations but typically charge monthly subscription fees of approximately AED 99. Additional charges may apply for foreign shareholders requiring enhanced verification.

Timeline expectations should be set realistically. For low-risk, UAE-resident-owned companies with straightforward documentation, traditional bank approval takes two to four weeks.

Non-resident founders, complex ownership structures, or businesses in sensitive activity categories should plan for four to eight weeks or more. Digital neobanks can approve eligible applications in three to ten working days, making them a practical choice where operational urgency exists.

The most consistent advice from businesses that have successfully navigated the Dubai banking process is to approach it as a strategic exercise, not an administrative one.

Your bank account application is a credibility assessment. Banks are asking whether your business is real, whether its structure is transparent, and whether the financial flows it will generate are legitimate.

Businesses that present themselves clearly and completely tend to be approved. Those who submit incomplete files or rely on opaque structures do not.

Also Read: