A decade ago, a UAE-based SME owner seeking business financing faced a near-universal experience: a bank loan application that took weeks, a collateral requirement they could not meet, and a rejection that left them back where they started. Fintech was supposed to change this. In many ways, it has, but 2026 marks a more significant inflection point than the gradual improvements of recent years might suggest. The convergence of AI-driven credit decisioning, open banking infrastructure, embedded finance, and a maturing regulatory framework has produced something that genuinely deserves the word revolution: a credit environment in which UAE SMEs can access capital faster, more fairly, and with far less friction than at any previous point in the country's financial history.

For SME owners navigating this new landscape, the challenge is no longer simply finding a willing lender. It is understanding which of several rapidly evolving credit channels fits their specific situation and knowing how to position their business to make the most of what automated credit assessment has to offer.

The Scale of the Problem That Is Being Solved

To understand why the current moment matters, it helps to be clear about the scale of the financing challenge that UAE SMEs have historically faced. Despite contributing around 60% of the UAE's non-oil GDP and employing the majority of the private sector workforce, SMEs in the MENA region receive just 7% of total bank credit. The regional SME credit gap stands at an estimated $475 billion, a figure that reflects not a lack of creditworthy businesses, but a structural mismatch between the way traditional banks assess risk and the financial reality of how small businesses actually operate.

The conventional bank model has always been poorly suited to SME lending. It relies on historical financial statements, fixed collateral, long processing timelines, and credit scoring models calibrated for larger businesses. In the UAE, where many SMEs operate on 60 to 120-day client payment terms and where a significant proportion of businesses are relatively young, these requirements eliminate large numbers of creditworthy operators before the conversation begins. The automated credit revolution is not just a technology upgrade; it is a fundamental redesign of how creditworthiness is defined and assessed.

How AI-Driven Credit Assessment Works in Practice

The defining characteristic of the new generation of automated credit platforms is the shift from static, backwards-looking assessment to dynamic, real-time analysis. Where a traditional bank looks at two or three years of audited financial statements, an AI-driven credit platform looks at live transaction data, invoicing history, payment behaviour, client credibility, cash flow patterns, and in some cases even trade licence status and digital footprint.

In the UAE, this approach has been significantly accelerated by the maturation of digital infrastructure that makes this data accessible. Automated Emirates ID verification, trade licence checks, and Ultimate Beneficial Owner screening, processes that once required manual processing over days, can now run in minutes. The Central Bank of the UAE's Financial Infrastructure Transformation Programme has established modern payment rails and open banking frameworks that allow fintech lenders to access bank transaction data with appropriate consent, enabling a quality of credit assessment that simply was not possible three years ago.

The practical result for SME owners is that credit decisions, which once took weeks, now take hours, and in many cases are available the same day. Emirates NBD's enhanced digital trade finance platform, for instance, incorporates automated credit assessment using bank transaction history and offers same-day decisions on trade finance for eligible SME customers. For a business owner managing a time-sensitive procurement decision or a supplier payment deadline, that speed differential is commercially significant.

The Rise of Embedded Finance: Credit Where You Already Work

One of the most consequential developments in the 2026 UAE credit landscape is the rapid growth of embedded finance, credit integrated directly into the platforms SMEs already use to run their businesses. Rather than seeking out a lender separately, business owners are offered credit at the point of need, within the workflow where it arises.

A platform that processes an SME's invoices, manages supplier relationships, or hosts marketplace transactions already holds the data needed to make a credit decision, in real time. When an SME uploads an invoice to an embedded lending platform, that invoice becomes the basis for an immediate financing offer. Credit is accessed dynamically, without a separate application process.

In the UAE, this model is gaining significant traction across several sectors. Platforms, including Tabby for Business and Tamara Business, B2B extensions of the region's leading consumer Buy Now Pay Later providers, are embedding payment terms into free zone trade platforms and SME business networks. The UAE's B2B BNPL market reached $1.97 billion in 2026 and is projected to grow at a compound annual growth rate of 23.9% through to 2030, reaching $4.66 billion by the end of the decade. For SME owners in trading, retail, and services, these embedded credit products represent an accessible and increasingly mainstream financing option.

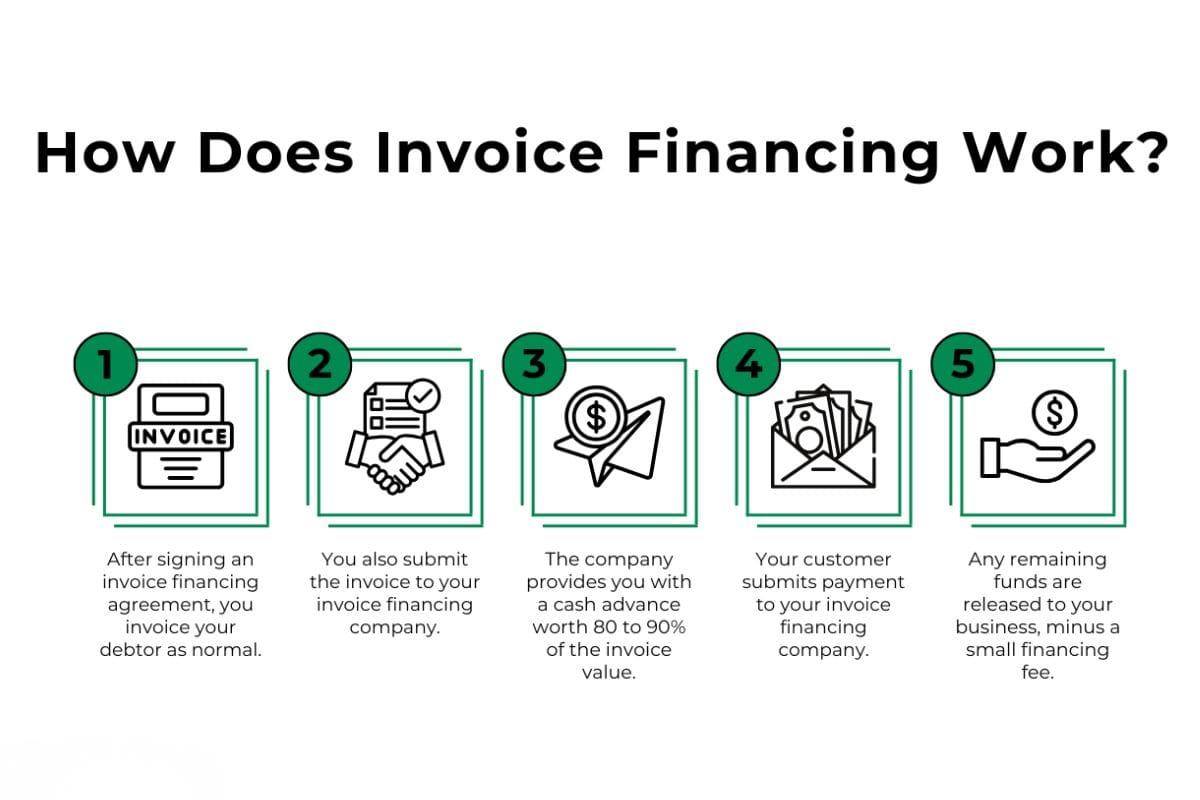

Invoice Financing and Working Capital: Unlocking Cash Already Earned

For many UAE SMEs, the most immediate financing challenge is not the absence of revenue; it is the gap between earning it and receiving it. Extended client payment terms of 60 to 120 days are standard across many sectors, and for a small business managing payroll, supplier costs, and operational expenses in the meantime, that gap can be the difference between growth and stagnation.

Invoice financing has been transformed by automated credit. Platforms like Aura Finance analyse invoicing history, payment timelines, and client credibility using AI-driven models to determine eligibility, often within hours. The business receives payment on the invoice date while the client continues using extended credit terms, with no collateral required and no equity dilution. For service businesses and B2B operators with strong client relationships but stretched payment cycles, this model addresses the core liquidity challenge directly.

The crowdfunding-adjacent working capital model is also gaining ground. UAE-based fintech Gainz, which secured a seven-figure pre-seed round in 2025, enables SMEs to launch working capital financing campaigns within minutes through a Shariah-compliant, AI-underwritten platform that allows investors to contribute capital from as little as $500. This broadening of the capital supply side expands the total pool of available credit and introduces competitive pressure that benefits borrowers.

The Regulatory Framework: Innovation with Guardrails

The speed of change in UAE SME lending has been matched by a regulatory environment that has, for the most part, kept pace with innovation. This is not accidental; it reflects a deliberate policy choice by the UAE government to position the country as a regional fintech leader while maintaining the safeguards that protect SME borrowers.

The DFSA updated its lending and credit rules in 2024 to include digital B2B lending within its regulated activity categories, providing fintech lenders in DIFC with a clear licensing pathway. The ADGM sandbox has enabled fintech startups to test AI-powered lending solutions in a controlled environment before full market launch; a framework described as allowing financial innovation to move from concept to market faster than anywhere else in the region. The UAE Ministry of Economy has also published SME financing guidelines recommending minimum standards for digital lending products, including cost transparency requirements that protect borrowers from opaque fee structures.

For SME owners, this regulatory maturity matters practically. Fintech lenders in the UAE are increasingly subject to the same standards of oversight as traditional banks, providing borrower protection that was not uniformly present in the market's earlier phase. When evaluating a digital lending product, checking for DFSA, ADGM, or Central Bank authorisation is a straightforward and important step.

How SME Owners Should Position Themselves

Understanding the new credit landscape is only half the equation. The other half is positioning your business to benefit from it. Automated credit platforms assess creditworthiness through data, which means the quality and accessibility of your business data is now a genuine competitive advantage when seeking financing.

- Keep your financial data clean and current

AI-driven credit platforms assess your business through transaction data, invoicing patterns, and cash flow behaviour. Businesses using cloud accounting software that integrates directly with their banking and invoicing workflows present cleaner, more accessible data profiles and receive faster, more favourable credit decisions as a result.

- Maintain a consistent digital trade history

Regular, documented transaction flows, consistent invoicing, prompt supplier payments, and reliable client collections build the kind of digital credit profile that automated platforms reward. Erratic cash flows and undocumented transactions work against you in an environment where the algorithm is forming its own view of your creditworthiness.

- Engage with your bank's digital SME products proactively

Traditional banks, including Emirates NBD and Abu Dhabi Commercial Bank, have both developed digital trade finance products for SME customers, incorporating automated assessment. These products are not always prominently marketed. Proactive engagement with your business banking relationship manager is often the most efficient way to discover and access them.

- Explore embedded credit at the platform level

If your business operates through a marketplace, procurement portal, or logistics platform, check whether that platform offers embedded financing options. The credit available through platforms where you already have a transaction history is often faster to access and more favourably priced than credit sought independently, because the platform already has the data needed to make a confident decision.

For UAE SME owners, the practical message is straightforward: the capital is more accessible than it has ever been, the platforms to access it are more numerous and more legitimate than at any previous point, and the businesses that understand how automated credit assessment works will be significantly better positioned to use it. The revolution is already underway. The question is whether your business is ready to benefit from it.

Also Read: